4 fabulous reasons to contribute to your ISA this Christmas

Each year, many investors end up rushing to make their ISA as the tax year draws to a close. But, to maximise the potential for growth, the savviest often open and contribute to their ISA early.

If you haven’t already maximised your ISA contributions, the festive season may present the perfect opportunity to get organised and beat the rush to top up your ISA.

Every UK individual has an annual ISA subscription, allowing you to save or invest up to £20,000 tax-efficiently in the 2023/24 tax year. This annual cap limits the amount you can contribute to your ISA.

As you're not allowed to carry it forward to the following year, if you don’t use your full allowance you lose it.

The latest government statistics show that Brits contributed around £72 billion to adult ISAs in 2020/21, with 12 million adult ISAs opened and subscribed to[1].

So, if you’ve yet to maximise your ISA this tax year, here are four smart reasons to act sooner rather than later.

1. Make the most of tax savings

Saving into an ISA is among the most tax-efficient ways to boost your wealth.

You can save into a Cash ISA and won't have to pay any Income Tax on the interest you earn on your savings. With the Bank of England base rate at 5.25% in November 2023, this may be something you need to watch out for[2].

Alternatively, investing in a Stocks and Shares ISA means you won’t pay any Income Tax or Capital Gains Tax (CGT) on any returns your ISA generates.

If you’re a higher- or additional-rate taxpayer, you’ll pay CGT at a rate of 20% on any gains you make on non-ISA investments above your annual exemption (£6,000 in 2023/24). So, the tax efficiency ISAs offer makes them a very attractive way to build wealth.

2. Gain more potential for growth

Deposit money in your ISA over Christmas and you’ll gift yourself extra time to enjoy potential growth on your investment.

While it may not be the start of the tax year, paying into a Stocks and Shares ISA early can make a significant difference to the returns you generate.

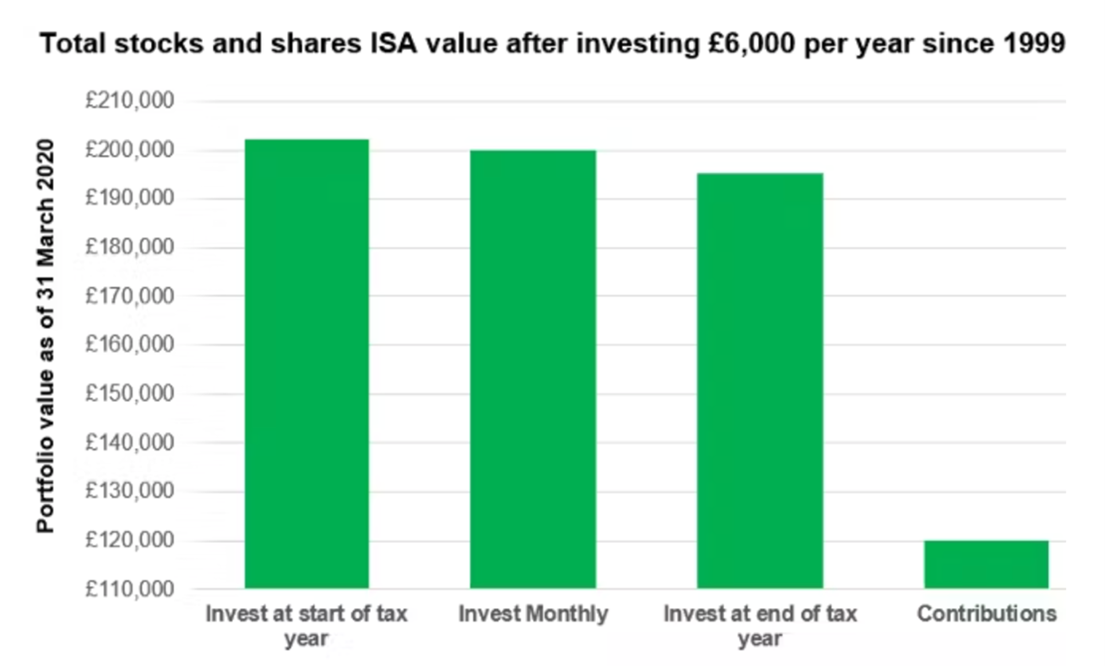

Nutmeg have helpfully calculated the difference that investing early could make. Their study revealed that if you invested £6,000 into a medium-risk Stocks and Shares ISA on the first day of the tax year between 6 April 1999 and 31 March 2020, your returns would be £6,969 greater than if you had waited until the final day of the tax year.

The chart below illustrates the difference in wealth growth.

Source: Nutmeg[3]

Making your contribution early means that you benefit from compounding on investment returns. And allowing your wealth the opportunity to be invested for longer could make a sizeable difference to the amount of growth that you see.

So, each tax year, the sooner you start saving into your ISA the more time your investments have to enjoy potential growth.

3. Benefit from pound cost averaging by drip-feeding money into your ISA

If you don’t have a large lump sum to invest, you could consider setting up a regular monthly payment into a Stocks and Shares ISA.

Drip-feeding your money into the market in this way helps you to spread your investment, allowing you to take advantage of “pound cost averaging”.

Due to market fluctuations, the value of investments rise and fall. As a result, when you invest regularly, you’ll buy shares or fund units at different prices. When prices rise, your money will buy fewer shares. Conversely, when prices fall, your money will go further and buy you more shares or units.

There's no guarantee that investing small sums regularly will achieve better returns than investing a lump sum, but you will end up paying the average price of the share. This helps to reduce your risk, providing you with potentially smoother returns.

4. Maximise tax-efficient saving by making ISAs a family affair

ISAs are “individual”, and you can only open one in a single name. Yet, if you have a spouse or partner, combining your allowance can be a great way of building up tax-efficient savings.

Between you, it’s possible to tax-efficiently save and invest up to £40,000 (in the 2023/24 tax year).

In the event that you’ve already maximised your own ISAs, if you have children or grandchildren under the age of 18, you could consider making use of a Junior ISA (JISA).

For the 2023/24 tax year you can pay up to £9,000 into a JISA for a child under the age of 18, and benefit from the same tax-efficient growth.

Saving through a JISA means you could tax-efficiently save and invest an additional £9,000 on top of your own ISA allowance.

If you don’t know what to buy for your child or grandchild for Christmas, setting up a JISA could give them a valuable and long-lasting gift that they can benefit from in the future.

Get in touch

If you’d like to find out more about how you could use ISAs to help you achieve your financial and lifestyle goals, please get in touch.

Email info@aspirafp.co.uk or call us on 0800 048 0150.

Please note

The information contained in this article is based on the opinion of Aspira and does not constitute financial advice or a recommendation to any investment or retirement strategy.

You should seek independent financial advice before embarking on any course of action.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

[1] https://www.gov.uk/government/statistics/annual-savings-statistics-2022/commentary-for-annual-savings-statistics-june-2022#individual-savings-accounts-isas

[2] https://www.bankofengland.co.uk/monetary-policy-summary-and-minutes/2023/november-2023

[3] https://www.nutmeg.com/nutmegonomics/the-early-isa-investor-catches-the-returns

Back To List

Submit a comment