5 common Inheritance Tax myths you shouldn't believe

Inheritance Tax (IHT) is contentious.

For some, it’s seen as the most hated tax. Appropriating someone’s assets on their death that may already have been subject to taxation during their lifetime is, to some, outrageously greedy.

On the other hand, proponents see IHT as an effective way to redistribute wealth from the richest families, allowing funds to be fed into supporting essential services such as education and health.

As well as being controversial, the details relating to IHT can also be subject to confusion and misunderstanding.

With more people potentially becoming liable for IHT as thresholds are frozen while property prices continue to remain robust, it’s important for you to understand the facts around it.

Read about five common IHT myths, together with some simple ideas that could help you keep your liability to a minimum.

1. Only the very wealthy are affected by Inheritance Tax

Although the traditional view of IHT is that it’s usually paid by the very wealthy, the number of people affected by the tax is on the rise. Professional Paraplanner recently confirmed that the number of estates liable for IHT in the 2022/23 tax year was 41,000, up from 33,000 the year before[1].

In 2023/24, IHT will only be charged on the value of your estate that exceeds the nil-rate band of £325,000. There is also an additional nil-rate allowance of £175,000, if you leave your residential property to your children or grandchildren.

Because nil-rate bands have been frozen since 2009, and are likely to remain at the current level until at least 2028, more estates are becoming liable for IHT.

With property values remaining resilient, it’s likely that an increasing number of people who would not describe themselves as wealthy could get caught in the IHT trap.

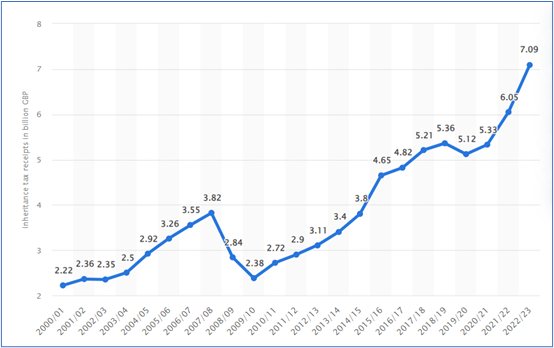

2. Inheritance Tax is a big income generator for the government

There’s a common belief that IHT is a big cash cow for the government, which then feeds the narrative that they won’t reform it because it is so lucrative.

As you can see from the chart below, apart from one blip in 2019/20, IHT receipts have been rising steadily since 2009/10.

In the last tax year, £7.1 billion was paid in IHT – an increase of £1 billion from the previous year:

Source: Statista[2]

However, as a percentage of overall HMRC revenue, the amount is relatively low.

Government figures confirm total tax revenues of £788.8 billion in 2022/23[3], meaning that the amount received in IHT was less than 1% of the total collected.

It’s also a relatively low figure compared with other revenue. For example, the same government figures reveal that receipts from tax on tobacco products totalled £10 billion in 2022/23 and the figure for alcohol duty was more than £12 billion.

3. I can pass all my wealth to my partner to avoid Inheritance Tax

To be fair, there is a certain element of truth in this common myth.

It is true that, if you leave all wealth to your spouse or partner in your will, they will not be liable for any IHT on your death.

However, that does depend on you having made a will specifying that all your assets should pass to them. Otherwise, your estate will be subject to the intestacy laws which could result in your spouse only receiving a proportion of your assets.

More importantly, leaving the value of your assets to your spouse or partner may only defer any potential IHT liability on the value of your estate until after they die.

While your nil-rate band allowances will pass to them on your death, that will still mean that the value of any assets above your combined nil-rate bands could be liable for IHT.

4. I can only gift £3,000 each year to reduce my Inheritance Tax liability

When you’re thinking about gifting your assets to reduce your IHT liability, these will generally fall under three separate categories:

1. Gifts that are immediately exempt from IHT

You and your partner can each make an annual gift of £3,000 each tax year that will not be included in the value of your estate for IHT purposes.

In addition to this exempt amount, you can both also make further gifts of up to £250 to as many other people as you like in any tax year.

If you’re a parent, you can both make a wedding gift to each of your children of £5,000. Grandparents can gift up to £2,500 each. You can gift up to £1,000 as a wedding gift to anyone else.

You should also note that there is no limit on the amount you can donate to charity each year.

2. Potentially exempt transfers

In reality, there is effectively no limit on the value of gifts you can give, but with the important caveat that those in excess of the allowances you’ve already read about are potentially exempt transfers (PETs).

All PETs are subject to the “seven-year rule” which means that IHT may be payable if you die within seven years of making the gift.

3. Gifts out of income

In addition to one-off amounts, you can also make regular gifts out of your annual income, with the advantage that these are immediately exempt from IHT.

These gifts could be used by a relative for a specific purpose, such as to cover living costs at university, or care home fees.

There are strict guidelines about gifts of this kind. The gift must be out of your normal income rather than from savings, and making the regular gift should not have a detrimental effect on your own standard of living.

Whenever you’re using gifting to help reduce or mitigate IHT, it’s important that you keep detailed records of any gifts you make – including the date and the amount gifted.

5. I can avoid Inheritance Tax by putting assets in trust

When you put money and assets into a trust, you are giving up your right to them. This means they have left your estate and the value may not be counted for IHT purposes.

However, for certain types of trust, the seven-year rule you read about earlier still applies. This will mean that if you die within seven years of transferring assets into trust, your estate could be liable for IHT at 40% of the value.

Using a discretionary trust could avoid this. It’s important to understand the rules surrounding trusts to ensure you’re making the right decision for you and your beneficiaries. So, we always recommend you work with a financial planner and a trust expert to help you achieve your estate planning goals.

Whatever types of trust you use, there are other taxes on assets that may be applicable. These could include a 20% charge when setting up the trust, and a “periodic” charge of 6% every 10 years from the date the trust was set up.

Assets such as money, land, or property could also be subject to an exit charge of 6% when they are taken out of the trust.

You need to be aware that, once assets are in trust, you have no say over what happens to them. So, in the event of any potential change in your circumstances, you will be unable to access them.

As you can appreciate, trusts can be a complicated issue, and we would strongly recommend you get expert advice.

Get in touch

If you’d like to talk to us about your estate planning and how to mitigate your IHT liability, please get in touch. Email info@aspirafp.co.uk or call us on 01454 632 495.

Please note

The information contained in this article is based on the opinion of Aspira and does not constitute financial advice or a recommendation to any investment or retirement strategy.

The figures and information in this article are based on current tax legislation (as of September 2023) and may be subject to change.

The Financial Conduct Authority does not regulate estate planning, tax planning or will writing.

For taper relief/PETs

Remember that taper relief only applies to gifts in excess of the nil-rate band. It follows that, if no tax is payable on the transfer because it does not exceed the nil-rate band (after cumulation), there can be no relief.

Taper relief does not reduce the value transferred; it reduces the tax payable as a consequence of that transfer.

You should seek independent financial advice before embarking on any course of action.

Approval Number - 191

[1] https://professionalparaplanner.co.uk/people-paying-iht-doubles-since-2019/

[2] https://www.statista.com/statistics/284325/united-kingdom-hmrc-tax-recei...

[3] https://www.gov.uk/government/statistics/hmrc-tax-and-nics-receipts-for-....

Back To List

Submit a comment